Agenda item

Hyndburn Leisure Financial Monitoring Position Qtr2 - April to September 2025/2026 and Payment of Annual Financial Subsidy for 2025/2026.

In accordance with Regulation 11(1) of the Local Authorities (Executive Arrangements) (Meetings and Access to Information) (England) Regulations 2012, approval is being sought from Councillor Noordad Aziz, Chair of the Resources Overview and Scrutiny Committee, to the following key decision is being made by Cabinet on 3rd December 2025, under the Special Urgency provisions, on the grounds that the decision is urgent and cannot reasonably be deferred.

Report attached.

Minutes:

In accordance with Regulation 11(1) of the Local Authorities (Executive Arrangements) (Meetings and Access to Information) (England) Regulations 2012, approval was granted by Councillor Noordad Aziz, Chair of the Resources Overview and Scrutiny Committee, to the following key decision being made by Cabinet on 3rd December 2025, under the Special Urgency provisions, on the grounds that the decision was urgent and could not reasonably be deferred.

The Cabinet considered a report of Councillor Melissa Fisher, Deputy Leader and Portfolio Hoder for Housing and Regeneration, providing an update on Hyndburn Leisure’s financial performance up to the end of September 2025 for the current financial year and seeking approval to pay a grant of £700,000 to that organisation in respect of the period 1st April 2025 to 31st March 2026.

Councillor Fisher provided a brief introduction to the report, outlining the forecast underspend of Hyndburn Leisure at the end of the financial year, as well as the risks if the Council did not provide the subsidy proposed. She remained satisfied that the Trust provided sustainable and cost effective leisure provision. In addition, the forecast for future years anticipated a gradual reduction in the subsidy required.

Councillor Dad indicated that there would be a further report early in the New Year about how Hyndburn Leisure and the Council were working together. The aim was to ensure that the Trust was sustainable after Local Government Reorganisation and would provide value for money for the taxpayer. Hyndburn Leisure had already demonstrated that it was on the right trajectory with the subsidy reducing from £1m in 2024/25 to £700k proposed in 2025/26. Monthly meetings were now taking place between Hyndburn Leisure, the Portfolio Holder for Resources and Council Operations and the Executive Director (Resources).

Martin Dyson, Executive Director (Resources), confirmed that the political administration was working closely with the Hyndburn Leisure to support its sound financial management. Councillor Fisher added that she now had greater confidence in the operation of the Leisure Trust and that its future had been enhanced by the opening of the new Cath Thom Leisure Centre.

Councillor Khan supported the provision of the subsidy, particularly given the health challenges faced by Hyndburn’s population. He noted the reduction in the level of subsidy for this year and the forecast reduction for future years and also queried the following matters:

- Whether the anticipated savings would be financed by increased revenue, or through lower energy, buildings and staffing costs;

- Whether more details of the new relationship between Hyndburn Leisure and the Council would made available in the forthcoming report; and

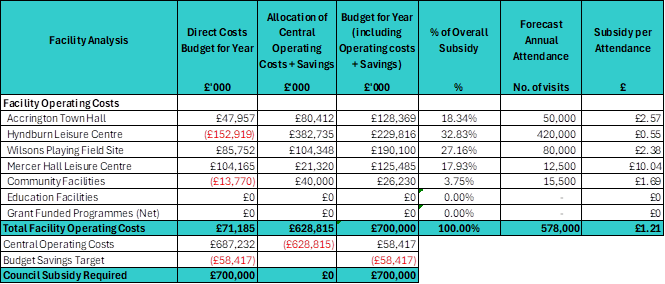

- Whether Hyndburn Leisure would be looking into the different levels of subsidy per attendance at its various venues (the Table provided at Paragraph 4.3 of the report refers).

Councillor Dad responded that the Council would continue to work closely with Hyndburn Leisure and to monitor its performance. The Council expected a health and well-being return on its investment. The report in the New Year would set out some key expectations upon Hyndburn Leisure. Clearly, the Council did not wish to see the Trust fail, but could not provide unlimited financial support for its future operations. Councillor Alexander confirmed that the details requested by Councillor Khan would be addressed in the forthcoming report as part of the Council’s overall approach. She added that the Council was not able to dictate what Hyndburn Leisure did operationally, but could influence it through maintaining a positive relationship and encouraging good working practices.

Regarding the question about subsidies attributable to each venue, Mr Dyson added that the facilities mentioned were being looked at on a site-by-site basis, although it was recognised that some buildings were not as efficient as others. It was acknowledged that attendance at Mercer Hall had fallen significantly, but the process of repurposing the site was still on-going. It was envisaged that there would be some evidence of improvement across sites by the time of the Quarter 3 monitoring report. The Trust continued to make efficiency savings, including the renegotiation of utility contracts. Also, the current report did not take into account the performance of the Cath Thom Leisure Centre, which was doing well.

Councillor Fisher indicated that four new trustees had been added to strengthen the Board, which was due to meet next Thursday, 11th December 2025.

Approval of the report was deemed a key decision.

Reasons for Decision

Proposed Grant - General Background

From its inception until 2021/22 the Council had paid an annual grant to Hyndburn Leisure to support its operating costs and the provision of pay and play sport and recreational facilities in the Borough. In 2008/09 Hyndburn Leisure had received £1.2 million in grant funding from the Council. However, as part of its response to the Government’s austerity measures, the Council had encouraged Hyndburn Leisure to become financially self-sufficient and, by 2021/22 the subsidy had reduced to nil. Since then, Hyndburn Leisure had faced significant financial pressures in common with leisure providers nationally. These cost pressures included:

- Significantly increased energy costs;

- increased staffing costs;

- inflation rate increases leading to higher supplier, maintenance and repair costs;

- increases in irrecoverable VAT; and

- lost income as a result of the partial closure of Mercer Hall Leisure Centre.

These cost pressures had resulted in a need for subsidy, with £235k being paid to Hyndburn Leisure by the Council in 2022/23 (before the Subsidy Control Act 2022 came into force), £490k being paid in 2023/24 and £1m paid 2024/25. A further subsidy had now been requested by Hyndburn Leisure in respect of the current financial year to enable pricing levels, opening hours and service provision to be maintained at the current level. It was considered that this would support the Council’s objective of supporting affordable and locally accessible health and wellbeing provision to help address the health inequalities in the Borough.

Proposed Grant - Subsidy Control

The proposed grant to Hyndburn Leisure would qualify as a subsidy for the purpose of the Subsidy Control Act 2022 (“SCA”) as it met the definition of a subsidy, namely:

- The payment would be given directly or indirectly from public resources by a public authority;

- It would confer an economic advantage on one or more enterprises, namely Hyndburn Leisure;

- Benefit would be gained by the enterprise receiving the grant over one or more other enterprises with respect to the provision of goods or services; and

- The grant would or was capable of having an effect on competition or investment within the UK.

Furthermore, as the provision of community leisure activity was typically viewed as an important health and wellbeing benefit for the community, Hyndburn Leisure could be considered to provide “services of public economic interest” (“SPEI”) pursuant to section 38 SCA as its services were:

- provided for the benefit of the public; and

- would not be provided, or would not be provided on the terms required, under normal market conditions.

The Council had already deemed Hyndburn Leisure to provide “SPEI” services and had provided SPEI subsidy to Hyndburn Leisure up to the £725,000.00 SPEI subsidy threshold (below which subsidy could be provided without a compliance assessment), having already paid subsidy to Hyndburn Leisure as follows:

- 2022/23 – the sum of £235,000.00 (prior to the SCA coming into force.

- 2023/24 – the sum of £490,000.00; and

- 2024/25 – the sum of £1,000,000.00

As the SPEI subsidy paid to Hyndburn Leisure in the last 3 years was currently above the SPEI subsidy threshold, no further subsidy could be paid to Hyndburn Leisure without the same being assessed against the statutory subsidy control principles (as detailed in Paragraph 3.5 of the report)

The SCA imposed requirements on local authorities when they were considering providing a third party with a subsidy. If these requirements were not complied with then the subsidy would be unlawful and could be challenged in the Competition Appeal Tribunal. In particular, the Council would have to assess the funding request against the subsidy control principles in Schedule 1 to the SCA and satisfy itself that the proposed grant was consistent with these principles. The subsidy control principles were as follows:

- Did the subsidy support a policy objective of the Council?

- Was the proposed method of subsidy the most appropriate way to address the policy objective?

- What would happen if the subsidy were not provided?

- Would the subsidy change the economic behaviour of the beneficiary and achieve something which would not have occurred without it?

- Was the subsidy proportionate and designed to minimise any negative impact on competition?

- Were any negative effects outweighed by the positive impact of providing the subsidy?

In this regard a compliance assessment had been carried out and was attached at Appendix 1 to the report. This indicated that the proposed subsidy appeared to be consistent with the subsidy control principles, especially given Hyndburn Leisure’s status as a provider of SPEI services.

In accordance with section 29 of the SCA the Council would need to do the following in order to pay further subsidy to Hyndburn Leisure:

- Satisfy itself that the amount of the grant was limited to what was necessary for Hyndburn Leisure to deliver the SPEI services, having regard to its income and costs plus no more than a reasonable profit or surplus. Reasonable profits could be assessed through a benchmarking exercise comparing the profits achieved by similar public service contracts which had been awarded under competitive conditions.

- Ensure that the funding was given in a transparent manner pursuant to a written contract or grant funding agreement which clearly set out the terms of the subsidy, including:

o Details of the SPEI services in respect of which the subsidy was given;

o Details of Hyndburn Leisure as the enterprise which was tasked with providing the services;

o The period for which the services were to be provided;

o Details of how the amount of subsidy had been calculated; and

o The arrangements in respect of reviews and steps which might be taken to recover the grant (for example if the funding was found to be more generous than permitted and part or all of it had to be clawed back).

Under Section 33 of the SCA the Council would be required to publish details of the grant on the UK’s Subsidy Database within three months of a formal decision to provide it, and to maintain this record for six years. Under Section 70 of the SCA, any interested party who was aggrieved by the making of a subsidy decision might apply to the Competition Appeal Tribunal for a review of the decision. The challenge could be in relation to the Council not complying with the subsidy control requirements in the SCA, or on more general public law grounds, for example that the Council did not behave reasonably or rationally when deciding to provide the grant. If such a challenge was successful the Competition Appeal Tribunal could impose remedies under usual judicial review principles, including an order for the recovery of the unlawful subsidy with interest. The period in which a challenge could be made in relation to the provision of a subsidy was typically one month from the publication on the UK Subsidy Database.

Proposed Grant - General Public Law Considerations

The Council had power under section 19(3)(i) of the Local Government (Miscellaneous Provisions) Act 1976 (LGMPA) to contribute, by way of grant or loan, towards the expenses incurred or to be incurred by any voluntary organisation in providing recreational facilities which the Council had power to provide under section 19(1) of the LGMPA (which gave the Council power to provide, amongst other things, indoor facilities consisting of sports centres and swimming pools). “Voluntary Organisation” was defined at section 19(3) of the LGMPA as being “any person carrying on or proposing to carry on an undertaking otherwise than for profit”. On the basis that Hyndburn Leisure was a charitable company limited by guarantee, it was a “not for profit” company. The Council therefore had statutory power to make the proposed grant to Hyndburn Leisure.

In exercising this statutory power, the Council would have to act for proper purposes and in good faith. In other words, the Council would have to act for proper motives, take into account all relevant considerations, and ignore irrelevant matters. It must not act irrationally and must balance the risks against the potential rewards. Of particular importance in this instance was the Council’s fiduciary duty to ensure that the proposed grant was an appropriate use of Council funds and would provide genuine and tangible benefits for the community.

Proposed Subsidy Grant 2025/2026

In March 2025, Hyndburn Leisure had set a budget with a forecast deficit of £700,000, which included achieving a savings target of £58,417.

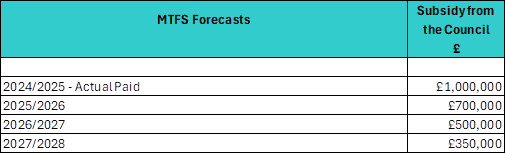

Hyndburn Borough Council had forecast the following subsidy payments to Hyndburn Leisure over the term of its Medium-Term Financial Strategy agreed by Council in February 2025.

Hyndburn Leisure had formally requested the payment of the subsidy for 2025/2026, and the table below showed the breakdown of the expected facility costs and cost of subsidy per attendance by site and the overall subsidy for the total annual attendances.

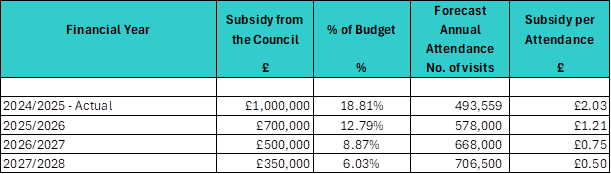

There was a reduction in the subsidy requested from £1m in 2024/2025 to £700,000 in 2025/2026 plus a forecast increase in annual attendances from 493,559 in 2024/2025 to 578,000 in 2025/2026.

This reduction in subsidy was largely due to the following factors:

- Late in 2024/2025 Hyndburn Leisure had taken over responsibility for procuring their own energy costs and were able to negotiate substantially reduced rates for the leisure centres than had been possible through the Council’s contract. This had resulted in a reduction in the kilowatt charge rate and the VAT rate, which had enabled savings of almost £300,000 per annum.

- As all costs had risen with inflation, Hyndburn Leisure had also renegotiated several of their other premises and supplies and services contracts and set a further savings target to be achieved in year to ensure the subsidy would be reduced from 2024/2025.

- The opening of the Cath Thom Leisure Centre in October would also contribute towards increased attendances, although in the first six months of operation the centre was not expected to make a financial surplus.

The financial support provided to Hyndburn Leisure would be used to make repayments against current year debts owed to the Council. This subsidy payment was expected to enable Hyndburn Leisure to meet all debts due to the Council for the financial year 2025/2026.

Rather than making a physical payment to Hyndburn Leisure for £700,000, the subsidy amount would be offset against the outstanding trading debt due to the Council.

Several other Local Authorities in Lancashire operated their leisure services under similar outsourced models and were also providing financial support to their leisure trust or leisure subsidiary companies. The level of financial support being provided by other Councils around Lancashire for 2025/26 ranged from £0.80million to £2million.

Hyndburn Leisure was currently in the process of developing its budget for 2026/27, and whilst it was still forecasting financial support would be required from the Council, this was expected to reduce from the current year subsidy requirement.

The future years’ subsidy targets had been agreed with the Council and were as follows:

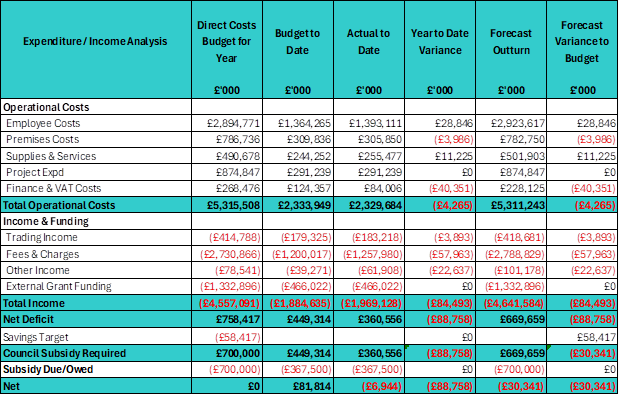

Financial Monitoring Position as at the end of September 2025

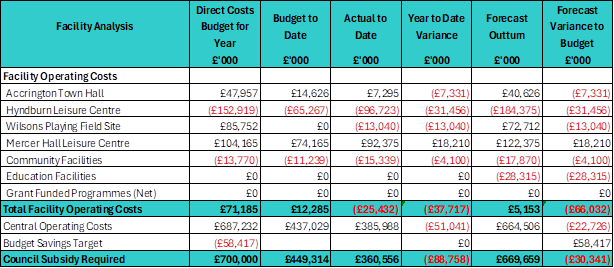

The current forecast net expenditure to the end of the financial year in March 2026 was £669,659. This brought the forecast underspend for the year against the budget to £30,341.

As shown in the table below the forecast underspend to date was shown by the facility operated, with most areas performing ahead of budget except for Mercer Hall which was currently closed due to the repurposing works.

Further analysis of the variances by Income and Expenditure type were shown in the table below:

The narrative below provided more detail on the variances from the original budget and the forecast outturn as at the end of September 2025.

Employee Costs

The forecast outturn position for employee costs showed an increase to the original budget of £28,846. This increase was mainly due to the increased NJC pay award of 3.2% that was 0.2% above the 3% budgeted in year.

Premises Costs

The forecast outturn position for premises costs showed a small underspend forecast of (£3,986) which was mainly due to energy efficiency savings through new contract rates and the new building management system installed at Hyndburn Leisure Centre.

Supplies and Services

The forecast outturn position for supplies and service costs showed an increase to the original budget of £11,225. This largely related to increased resaleable supplies that had been purchased and were offset by additional income forecasts.

Project Expenditure

The costs in this area reflected the income received and always net out to zero.

Finance & VAT Costs

The forecast outturn position for finance and VAT costs showed an underspend to the original budget of £40,351. This underspend related to savings / profit share from the operations at Accrington Academy and additional VAT savings as the new utility contracts only attracted VAT at 5%.

Trading Income - including Catering, Bar, Vending, Resale and Events

The forecast outturn position for trading income showed an increase to the original budget of (£3,191). This increase was made up of additional catering and resale items that partly offset the increased costs of supplies and services:

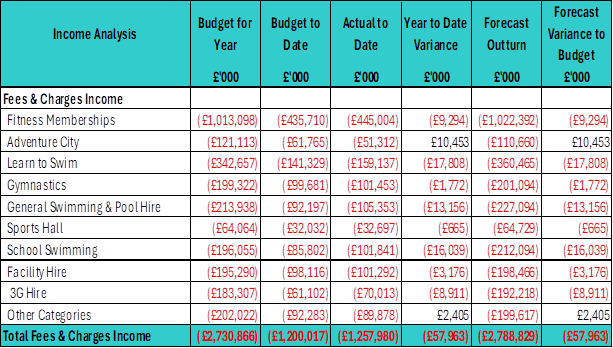

Fees & Charges Income – Memberships, Pay as You Go Activities, Facility Hire

The forecast outturn position for fees and charges Income showed an increase to the original budget of (£57,561). The table below showed the activities that had generated this increase.

Other Income – Service Recharges & Sponsorship

The forecast outturn position for Other Income showed an increase against the original budget of (£22,637). This increase was made up of:

a) Sponsorship received for the Hyndburn Sports Awards £6,900;

b) Recharges for supplies & services £9,984;

c) Cash in Transit / Bank Interest £11,317.

External Grant Funding – External Grants & Commissions

There were no variances on this funding.

Impact on Subsidy Required from the Council

As shown in the latest forecast, Hyndburn Leisure were forecasting a small underspend of £30,341 in year assuming the Council has paid the proposed subsidy of £700,000. If Hyndburn Leisure achieved an underspend in year, it would be prudent to allow them to retain any surplus as a reserve balance to cover any short-term cash flows and cover any unforeseen risks that might occur in future years.

Alternative Options considered and Reasons for Rejection

The Council could decide not to make the grant payment. The Council could also decide to pay a lesser amount than that requested by Hyndburn Leisure. However, either approach could result in Hyndburn Leisure raising prices, reducing its opening hours and / or reducing its services. In a worst-case scenario it might result in Hyndburn Leisure ceasing to operate and Cabinet was advised to seek further advice as to the likelihood and consequences of this occurring if it was minded not to pay the requested grant funding to Hyndburn Leisure or to pay a lesser amount.

Resolved (1) That Cabinet notes the forecast financial position of Hyndburn Leisure at Q2 of the 2025/2026 financial year as shown in Section 5 of the report.

(2) That Cabinet agrees to pay Hyndburn Leisure the sum of £700,000.00 by way of grant to support the provision of community leisure services in the Borough in respect of the period 1st April 2025 to 31st March 2026, subject to completion of a grant funding agreement in accordance with Paragraph 3.6 of the report.

Supporting documents:

-

Hyndburn Leisure Financial Monitoring Q2 - Main Report, item 241.

PDF 236 KB

PDF 236 KB -

Appendix 1 - Subsidy Control Assessment, item 241.

PDF 289 KB